Zakat on Retirement Accounts: A Complete Guide

For many Muslim families in North America and beyond, the largest concentration of wealth sits inside a retirement account. Whether that balance counts for zakat — and how to calculate it if it does — depends on a single principle that the classical tradition is clear about. This article applies that principle to every common retirement account type.

The Governing Principle: Complete Ownership

Zakat is not owed on wealth you do not fully own. The classical condition is al-milk al-tamm — complete ownership — which requires that you can possess the wealth, use it, benefit from it, and dispose of it without restriction, penalty, or a competing claim. This condition is recognized across all four Sunni schools of Islamic law.

A 401(k) during the accumulation phase (before age 59½) does not meet this standard. You cannot withdraw the funds without incurring a 10% federal penalty on top of ordinary income tax. You cannot gift or transfer the account outside the plan. You cannot use the balance for any purpose the plan structure doesn’t allow. Choosing between Fund A and Fund B within a locked account is not the kind of ownership — the qudrah ‘ala al-tasarruf, capacity for unrestricted disposal — that the classical tradition requires.

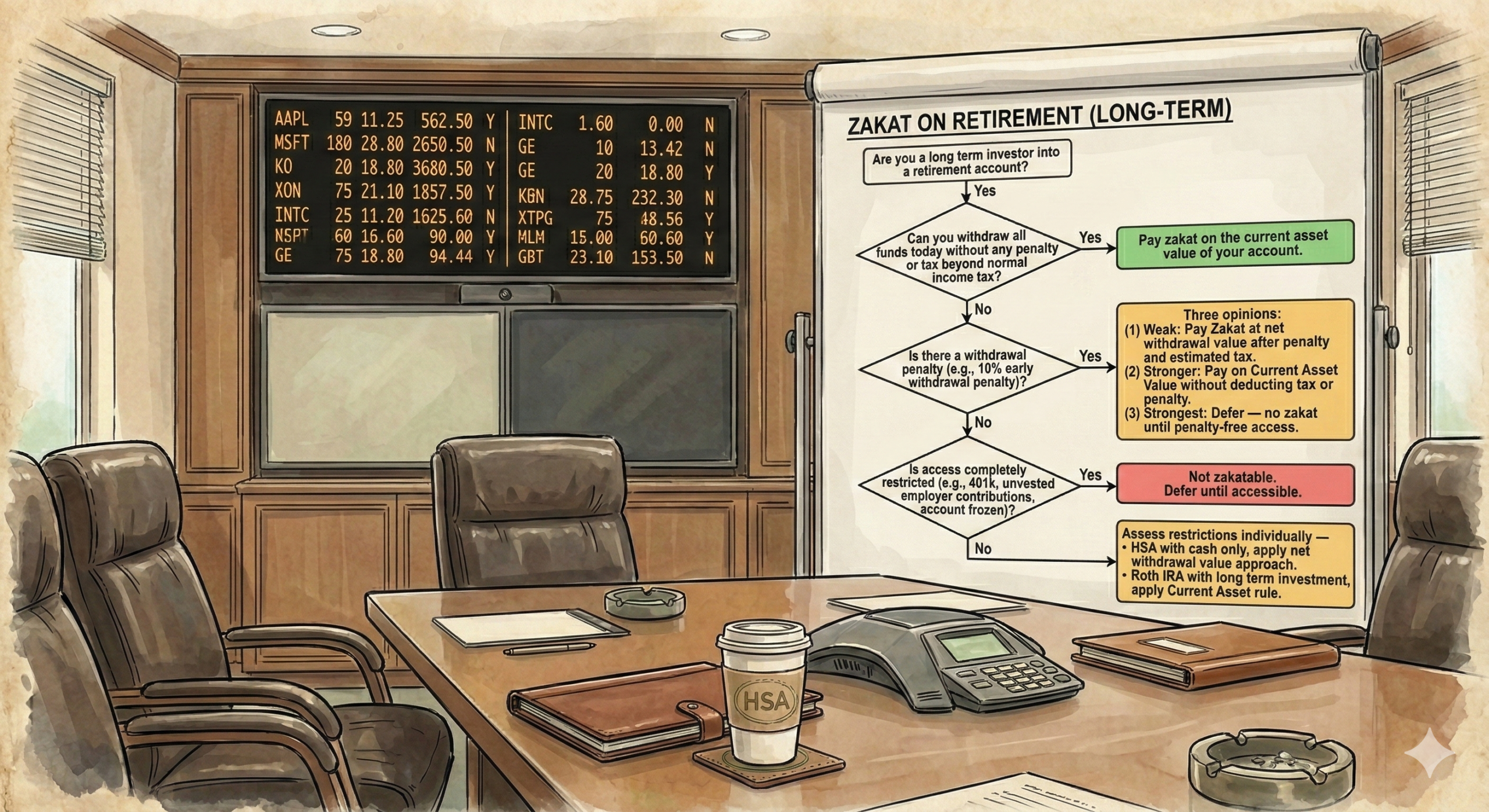

When an account is fully accessible without penalty, it is owned. When it is restricted by penalty, it is not fully owned. When access is completely blocked, there is nothing to calculate.

The Three Scholarly Positions

Three substantive positions exist on restricted retirement accounts:

Position 1 — Strongest: No zakat until withdrawal. Zakat is not obligatory on any restricted account until you actually withdraw the funds. At that point, you owe zakat for that year only, on what you received. This is the position I hold and explain below.

Position 2 — Stronger: Zakat on the net accessible value. The account is zakatable, but you may subtract the estimated 10% penalty and estimated income tax before calculating 2.5%. The problem with this approach is that it assumes a withdrawal you are not making, deducting costs that will only materialize if you actually withdraw.

Position 3 — Weak: Zakat on the full balance. Some scholars treat the account as fully owned regardless of restrictions and assess 2.5% on the total balance. This position does not engage with the ownership condition in the way the classical sources require.

My position is Position 1. The International Islamic Fiqh Academy’s analysis of end-of-service benefits is instructive: the employee has a contractual entitlement, the funds are allocated in their name, but they do not have full ownership because they cannot control the funds. The Academy’s resolution states that zakat is not obligatory on such amounts "throughout the service duration because the employee does not have full ownership." The American 401(k) before age 59½ is structurally identical.

Account-by-Account Breakdown

Traditional 401(k), 403(b), 457(b)

Pre-tax contributions, tax-deferred growth, restricted access before 59½ with a 10% early withdrawal penalty plus ordinary income tax.

Under Position 1: no zakat during accumulation. When you begin taking distributions at retirement, include each distribution in your zakatable assets for that year.

Under Position 2: pay zakat each year at the Current Asset Value without deducting your effective tax rate or the penalty, then apply 2.5% to that amount.

A 457(b) (common for government and nonprofit employees) generally has no 10% early withdrawal penalty upon separation from service — check whether your specific plan imposes restrictions.

Roth 401(k) and Roth IRA

Contributions are after-tax. Contributions to a Roth IRA can be withdrawn at any time, at any age, without penalty or tax. Earnings, however, are subject to restrictions until age 59½ and a five-year holding period.

Contributions: Fully accessible, fully owned. Zakatable at Current Asset value.

Earnings (before qualifying distribution): Restricted. Apply the same analysis as a Traditional 401(k).

Earnings (after age 59½ and five-year holding period): Fully accessible. Zakatable at Current Asset value.

Practically: if your Roth IRA has a contribution basis of $40,000 and total value of $65,000, the $40,000 is zakatable. Pay on the Current Asset value of the $40k (approximately 30% = $12,000), so your Zakat due is $300. The $25,000 in earnings is deferred under Position 1 until qualifying distributions begin.

Traditional IRA

Same analysis as the Traditional 401(k).

Health Savings Account (HSA)

An HSA is triple tax-advantaged — contributions are pre-tax, growth is tax-free, and distributions for qualified medical expenses are tax-free. Non-medical withdrawals before age 65 carry a 20% penalty plus ordinary income tax.

While the HSA is restricted for non-medical early withdrawal, you are still able to spend freely from the HSA for your healthcare expenses, like you would with your debit card. If you have built a large HSA balance as an investment vehicle, apply the long term passive investment method using the CRI / Current Assets / 30% rule method.

529 (Education Savings Plan — USA)

529 plans restrict distributions to qualified educational expenses. Non-qualified withdrawals trigger income tax plus a 10% penalty on earnings.

The standard position is to defer zakat on 529 funds until spent on qualified education expenses, therefore pay 2.5% on your withdrawal when you make them.

RRSP (Canada — Registered Retirement Savings Plan)

Functionally equivalent to the Traditional IRA or 401(k). Contributions are pre-tax, growth is tax-deferred, and early withdrawal is subject to withholding tax and full inclusion in taxable income. The RRSP converts to an RRIF at age 71, at which point you must begin taking minimum annual withdrawals.

Under Position 1: defer zakat during accumulation. When RRIF distributions begin, include each year’s distribution in your zakatable wealth for that year.

RESP (Canada — Registered Education Savings Plan)

An RESP is restricted to educational purposes for the named beneficiary. The standard position is to defer zakat on RESP funds. When a beneficiary makes educational withdrawals (Educational Assistance Payments), those flow to the student as taxable income — at that point, if the student has other zakatable wealth, the withdrawn funds are assessed as part of their individual calculation.

TFSA (Canada — Tax-Free Savings Account)

The TFSA is the cleanest case. Contributions are after-tax. Growth is tax-free. Withdrawals are penalty-free and tax-free at any time, for any purpose.

A TFSA is fully owned in the classical sense: you can access it today, for any reason, without cost. It is zakatable at full current value. If you are holding cash, include your entire TFSA balance in your zakatable assets. If you are investing long term, use the CRI / Current Assets / 30% rule method.

FHSA (Canada — First Home Savings Account)

The FHSA allows first-time home buyers to save and invest tax-free for a qualifying home purchase. Non-qualifying withdrawals are subject to income tax.

Under the ownership analysis, funds in an FHSA are restricted. Defer zakat on FHSA funds until a qualifying withdrawal is made or until the account is closed and proceeds transferred to an RRSP/RRIF. Pay 2.5% on your withdrawal.

Early Withdrawal Scenarios

If you withdraw from a restricted account before reaching the qualifying age or event, what is zakatable?

Under Position 1, the net proceeds — what actually enters your hands after penalty and tax withholding — are zakatable in the year of withdrawal. You do not owe back-zakat for all the years the money sat in the account.

When You Retire and Gain Full Access

When restrictions lift at retirement age, upon separation from service for certain plans, or at 65 for an HSA, the accounts become fully owned. At that point, the full balance enters your zakatable wealth.

- Your zakat obligation may increase significantly in the year of transition.

- Zakat on retirement distributions is charitable giving, which is often tax-deductible in the year you pay.

- If you are still in the accumulation phase and concerned about future liability, consider paying voluntary charity now in anticipation.

Summary Table

| Account | Penalty-Free Access? | SZG Default Position | Zakatable Amount |

|---|---|---|---|

| Traditional 401(k)/403(b) | No (before 59½) | Defer | At distribution |

| Roth 401(k)/Roth IRA — contributions | Yes | Zakatable now | Full contribution basis @ 30% |

| Roth 401(k)/Roth IRA — earnings | No (before 59½) | Defer | At qualifying distribution |

| Traditional IRA | No (before 59½) | Defer | At distribution |

| HSA | Yes for medical, No for non-medical. | Zakatable now | At distribution or age 65 |

| 529 | No (non-educational) | Defer | At qualified withdrawal |

| RRSP | No (heavy tax hit) | Defer | At RRIF distribution |

| RESP | No (restricted) | Defer | At EAP withdrawal |

| TFSA | Yes — always | Zakatable now | Full balance or 30% rule |

| FHSA | No (non-qualifying) | Defer | At qualifying withdrawal |