How We Calculate Zakat on Stocks

Paying zakat on stocks is one of the most common sources of confusion in contemporary zakat practice — and one of the most consequential in dollar terms. Get the method wrong and you either overpay by a factor of three or underpay by ignoring the obligation entirely. This article explains the method Simple Zakat Guide uses, why it is the correct method for most investors, and where the alternatives apply.

The Core Principle: Zakat Follows What the Company Owns

When you own shares of a company, you own a fractional interest in everything that company owns — its cash, its inventory, its factories, its patents, its brand. But those assets are not all zakatable. The classical tradition is clear: tools of production, fixed assets, and productive capital are not subject to zakat. You do not pay zakat on a hammer, a factory, or a server farm. These are the means by which wealth is generated, not wealth itself in the zakatable sense.

What is zakatable is the liquid, transactional layer of a company’s balance sheet — cash, receivables, and inventory. These are the assets that correspond to the categories of zakatable personal wealth: cash in hand, debts owed to you, and goods held for sale.

The market price of a stock reflects everything the company owns — including the factories, brand equity, and intellectual property that are not zakatable. Paying 2.5% on the full market price means paying zakat on a figure that includes large amounts of non-zakatable fixed assets. This is the fundamental problem with the full market value method for passive investors.

The Net Current Assets Method (The Mainstream Position)

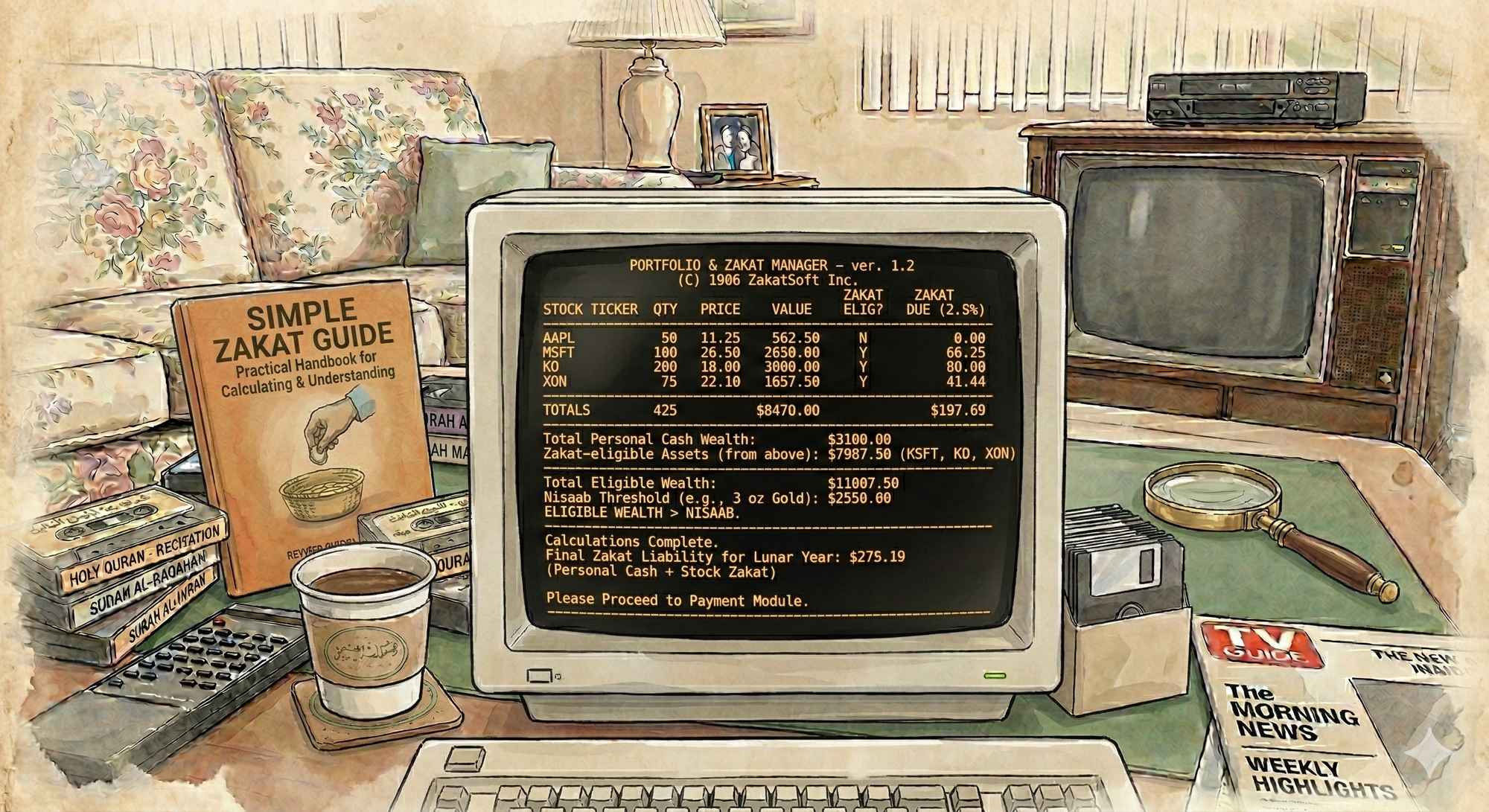

The Net Current Assets method — also called the CRI method (Cash, Receivables, Inventory) — calculates your zakatable share of a company’s liquid assets.

The formula:

(Current Assets − Current Liabilities) × (Your Shares ÷ Total Shares Outstanding) = Your Zakatable AmountWhat "current assets" means: Assets the company expects to convert to cash within one year — cash and equivalents, short-term investments, accounts receivable, and inventory. These are the liquid, transactional assets that map directly to the classical categories of zakatable wealth.

Why subtract current liabilities: You only own what is actually there after accounting for what the company currently owes. Paying zakat on gross current assets without netting out current liabilities would mean paying on wealth that is already spoken for by creditors.

Why current assets specifically, not total assets: Total assets include property, plant and equipment, long-term investments, intangibles, and goodwill — none of which are zakatable under any classical framework.

Where to Find the Data

A company’s current assets and current liabilities appear on its quarterly or annual balance sheet, available on:

- The company’s investor relations page (10-Q and 10-K filings)

- SEC EDGAR (edgar.sec.gov)

- Financial data platforms: Yahoo Finance, Morningstar, Macrotrends

Look for the most recent balance sheet date available at the time of your zakat calculation.

The 30% Proxy (When Company Data Isn’t Available)

Pulling a balance sheet for every stock in a diversified portfolio is impractical. For ETFs, index funds, and managed funds, calculating a look-through CRI for hundreds of underlying holdings is effectively impossible for an individual investor.

Research and analysis of S&P 500 companies over multiple years shows that the average ratio of net current assets to market capitalization for diversified equity portfolios tends to cluster around 25%–30%. Using 30% of market value as a proxy for the zakatable amount is conservative — it rounds up to ensure you are not paying less than you owe.

The 30% proxy formula:

Your Stock's Market Value × 30% = Zakatable Amount

Zakatable Amount × 2.5% = Zakat DueThis is the default method Simple Zakat Guide uses when processing equity holdings without individual balance sheet data.

When the 30% proxy applies:

- ETFs, index funds, or managed funds (no individual company breakdown practical)

- Individual stocks where you choose not to pull balance sheet data

- Foreign-listed stocks where financial data is less accessible

When to use actual company data instead:

- You hold a significant position in a single company

- You want maximum accuracy in your calculation

- The company is in a sector with unusual balance sheet structures (financials, utilities)

The Scholarly Positions

Three methods appear in contemporary fatwa literature.

The Dividend-Only Method

Some early contemporary rulings assessed zakat only on dividends actually received. This position is not broadly held in mainstream contemporary scholarship. When a company retains earnings rather than distributing them, those earnings still increase the company’s assets — and your proportional share of those assets. Paying zakat only on the fraction distributed is paying on a small slice of what you actually own.

Net Current Assets — The Mainstream Position for Passive Investors

This is the position Simple Zakat Guide applies. It is held by a broad range of contemporary scholars and institutions including many major fatwa bodies in the Muslim world and North America. It correctly applies the classical distinction between liquid zakatable assets and non-zakatable productive capital to the modern corporation.

Full Market Value — For Active Traders Only

If you are an active trader — buying and selling shares regularly, holding positions for days or weeks, treating shares as inventory rather than long-term investment — then shares are your merchandise. For a trader, the full market value of the portfolio on the zakat date is zakatable.

The distinction is one of intent and holding period. A long-term passive investor and a day trader own the same shares but for categorically different purposes. The zakatable amount differs accordingly.

Active vs. Passive: How to Know Which Category You Are In

You are a passive investor if you:

- Hold positions for more than a year

- Do not frequently buy and sell based on price movements

- Own index funds, ETFs, or mutual funds without actively managing individual positions

- Treat your portfolio as long-term wealth accumulation, not a trading business

You are an active trader if you:

- Buy and sell positions within days, weeks, or short months

- Hold shares specifically for short-term price appreciation

- Treat your portfolio as an income-generating trading operation

Most people with retirement accounts, brokerage accounts, or employer stock programs are passive investors. The net current assets method applies to them.

REITs: A Different Treatment

Real estate investment trusts (REITs) are structured as real property ownership vehicles — their assets are primarily real estate, not current liquid assets in the standard balance sheet sense. Applying the standard net current assets formula to a REIT will yield a misleadingly low result.

For REITs, the applicable analysis is closer to direct real estate ownership: the REIT holds properties for income generation, and those properties are not zakatable in their own right. Rental income distributed as dividends is zakatable in the year received.

Simple Zakat Guide uses the 30% proxy as a conservative approach when REITs appear in a portfolio, while acknowledging that a deeper analysis by a qualified scholar may yield a lower figure.

ETFs and Funds: Look-Through vs. Fund-Level

For an ETF holding hundreds of individual stocks, a full look-through calculation is impractical. Two approaches exist:

Fund-level proxy: Apply 30% of the fund’s market value as the zakatable base. This is Simple Zakat Guide’s default approach.

Look-through approach: Services like Zoya Finance calculate CRI values for many ETFs by aggregating underlying holdings. If you want precision, using their data for major index ETFs is a legitimate option and will typically yield a lower zakatable amount than the 30% proxy.

For fixed-income ETFs (bond funds), the treatment is different. The fund’s assets are debt instruments, which are impermissible to profit from. If you hold these, you must pay Zakat on the entire value of the fund and give away all the interest.

What About Unrealized Capital Gains?

For a passive investor, unrealized gains are not separately zakatable. The net current assets method already captures your proportional share of the company’s current wealth, which includes retained earnings and accumulated value.

When you sell shares, the full sale proceeds enter your liquid assets and are treated as cash from that point. All accumulated gains are captured at the point they become real, accessible money in your hands.

Calculating Inside Retirement Accounts

If you have determined that some or all of your retirement account is zakatable, the same stock calculation method applies to the equity portion. Identify the market value of the stocks or funds in the account, apply the 30% proxy or actual NCA calculation, and include the result as part of your zakatable assets.